Single Column Cash Book

Definition

A single column cash book is a book that lists only cash transactions and looks like any other cash account. All cash receipts are listed on the left in the cash book, and all cash payments are listed on the right. The single column cash book is also termed a simple cash book shaped like a T account.

The cashbook has two parts, the right side is called the credit side (payments), and the left side is called the debit side (Receipts). The “amount” column indicates the balance of transactions in each part.

Note:

It never shows credit balance and always takes debit balance or Nil balance.

Explanation

There are only listed cash transactions in single column cashbook. However, sometimes bank deposits and withdrawals are also recorded in cashbooks. All cheques received by the bank should be debited. On the other hand, all cheques presented for cash at the bank counter should be credited.

There are the following important ingredients of a cashbook:

- Cash Receipts (Debit)

- Cash payments (Credit)

- Single “amount” column on both sides

- Closing balance always debit or Nil

- Cash deposited and withdrawn from the bank

Format of a Single Column Cash Book

The shape/format of single column cash book is described in the following form:

To understand the meaning of both sides of the cashbook, the columns are explained below:

Date:

The Date column is used to record data for the year, month, and actual date of the listed transactions in cash book. This column appears on both Debit and Credit sides.

The actual date on which the cash was received is listed on the debit side in the first column and the actual date on which the cash was paid is listed on the credit side.

The important thing, however, is that there is no need to re-enter the year or month for additional entries unless a new month begins or a new page is required.

Receipts/payments: (Particulars)

This column is used to record all receipts/payment titles or details. On the debit side all receipts ‘title or description’ is listed. In a single column cash book, the credit side has the title or description of all payments. This column is also called “Details”. For example, the names of the parties (personal accounts), nominal accounts, real accounts, etc.

Note: –Generally, the receipts column on the debit side starts with balance b/d means cash in hand at the beginning of the year.

Voucher number: (Vr. No.)

This column is related to the serial number of the cash transaction. The serial number of all receipts is listed on the debit side and the serial number of all payments is listed on the credit side in the voucher column of the cashbook.

- When the payment is received, the payer keeps a copy of the receipt and the original one sent to the payee. This receipt is known as a debit voucher.

- When the payment is made, the payee keeps a copy of the receipt and the original one sends to the payer. This receipt is known as a credit voucher.

Ledger Folio: (L.F.)

This column is also used on both sides of the single column cash book. The ledger folio is used to record page numbers against every detail when entries are posted in the ledger account. This column is also used to confirm transactions in the cash book. It is also called page reference (P.R.).

Amount:

There is only one money column on either side of the cash book so it is called single column cash book. This column lists the amount of cash transactions during the year or month. The amount of cash received during the year/month is recorded on the debit side. Similarly, the amount of cash paid during the year/month is recorded on the credit side of the cashbook.

Example

Balancing the single column cashbook:

At the end of the month or accounting year, the sum of the columns on both sides is totaled. The total debt side of a cash book is always heavier than the total credit side. Because we cannot pay more than we received during the month/year.

The difference between both sides is called cash in hand which is written towards the credit side as balance c/d. Balance carried down(c/d) is the closing balance at the end of the month or accounting year. In the next month or year, this will become an opening balance, commonly referred to as Balance (b/d).

Solution:

Single column cashbook Ali&Sons company

Note: The entries on 10 & 12 April 2022 are not recorded in the cash book. Because goods purchased or sold on credit basis are not in the cash book.

Entries Explanation:

April-1: Cash in hand is the opening balance of the company. This would be closing balance (i.e balance c/d) on 30th April 2022.

April-4,8,14: Cash sales and the sale of old furniture in cash increases the company’s cash and is listed on the debit side of the cashbook.

April-18: Ali paid his loan to the company, also increases the cash, and recorded it on the debit side.

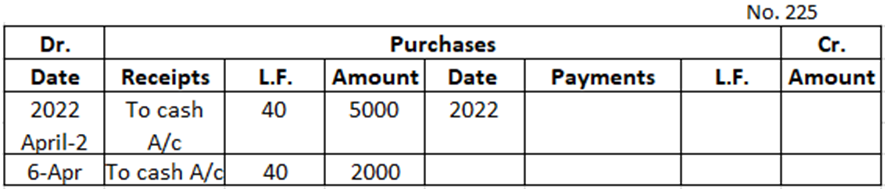

April-2,6: Goods purchased by the company for business will decrease the cash of the company and are recorded on the credit side.

April-3: Carriage paid has reduced the cash and recorded on the credit side.

April-16: Stationery purchased by the company for office use has also reduced the cash and recorded on the credit side.

April-17: Cash withdrawal for personal use (drawings) diminish the balance of the company and is recorded on the credit side.

Posting entries from single column cash book to ledger accounts:

The following steps should be kept in mind while transferring the entries from the cashbook to the relevant ledger account.

- The opening balance (balance b/d) and closing balancing (balance c/d) of the cashbook are not posted into the ledger account.

- The list of entries on the debit side is posted to the credit side of the relevant ledger account.

- The list of entries on the credit side is posted to the debit side of the relevant ledger account.

- The page number of the cashbook from which the entries are transferred to the ledger account is written in the ledger folio column. This will help in finding the relevant ones in the ledger.

- The ledger folio serial number is written on the right corner of each ledger account.

General Ledger of Ali & Sons Company:

2 Comments